Are You In Your 20s? You Have A Key To Financial Success That Everyone Else Does Not

When you get your first job or your first source of income, it is easy to postpone saving and investing as the stuff you will start working on once your income increases. This is because it is widely accepted that with age, our earning ability will increase – and this is often true. However, when you postpone the start of your saving and investing journey, you are losing the one asset you have in your twenties that the rest of us do not: time.

This post will demonstrate how time works to your advantage when it comes to long-term investing (even if you are investing in low-risk, low-return investments). My hope is that if you are in your twenties and reading this, it will convince you to start setting aside small amounts of money and investing them. I would like you to take advantage of this asset that you have.

First, starting later will not be as easy as you imagine

Yes, as you progress in your career or as you hone your craft you will make more money – this is expected. However, starting to save and invest then will not be as easy for two reasons:

Mathematically, you will have to save A LOT MORE to catch up on your long-term goals. Let us use a simple example of two people:

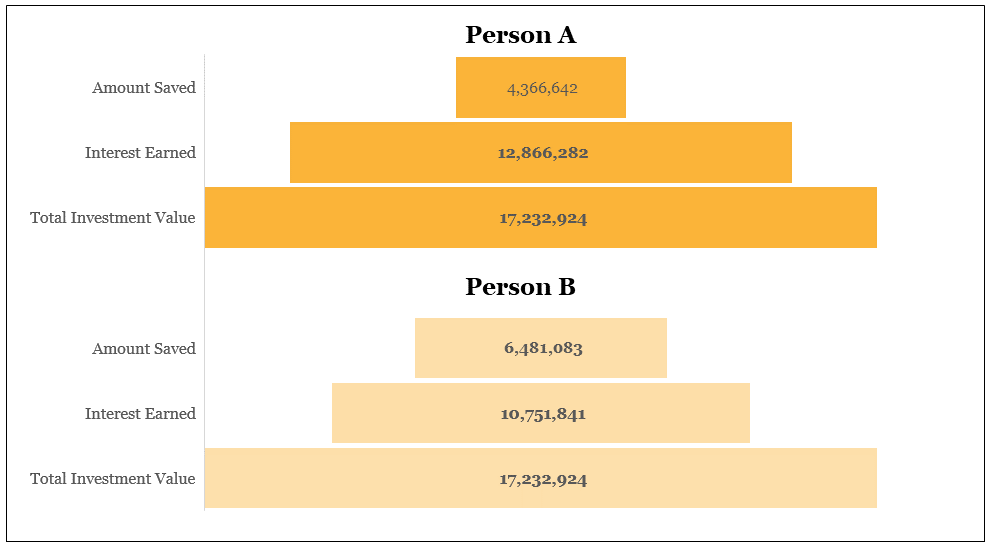

Person A: Starts saving at 25 when they get their first job. They are not earning much, but they are able to set aside KES 2,000 per month for the first year towards their long-term nest egg. As their income grows, they grow their saving rate by 10% annually. So year 2 of employment they are saving 2,200 shillings per month, and so on and so forth. Assuming this person is investing at 12% per year (which is fairly conservative if we are thinking long-term), this small fund will have grown to KES 17.2 million by the time they are 55. A decent nest-egg even if you factor in inflation. Remember, this person started with 2,000 shillings, what their age mates easily spend on a night out.

Person B: Gets caught up with moving out of home, getting married, buying their first car, enjoying life with friends etc with the hope that they will start saving for the long-term, once they “settle down”. They eventually settle down at 35 and want to start saving. For this person to end up with a nest egg of the same size as Person A by the time they are 55, they will need to start saving KES 8,439 per month and keep growing this saving by 10% annually. That is four times the savings. You may argue that their income will be four times more, but do not forget, so are their expenses. While 2,000 is what one spends on a night out, 8,500 bob is substantial – someone’s fuel bill for a month. That 10% growth rate is also no joke when you start with a high amount. By the time they are 45, they will need to be saving 22,000 shillings per month (Person A will need to save only 13,ooo shillings at the same age)! Finally, this person will be nurturing a new habit at a point where there are so many demands on their money.

Which of the two people is more likely to have that retirement nest egg?

Secondly, there is a magical thing we call compound interest

In high school, we did some money math about compound and simple interest. Simple interest is easy to compute. Say you invest 2,000 shillings for 5 years, at 12% simple interest. Your earnings will be your investment, multiplied by the interest rate, multiplied by the period:

2,000 * 12% * 5 = 1,200

So should you cash out, you will get 3,200 shillings at the end of five years.

Compound interest is a bit more complicated. The money you earn each year is reinvested at the same interest rate. Using the same example, your compound interest returns look like this:

Year 1: 2,000*12% = 240

Year 2: 2,240*12% = 268 (the principle in year 2 is the 2,000 you invested, plus the 240 it earned you in year 1)

Year 5 3147*12% = 377

If you cash out at year 5, you get a lot more money: 3,524 shillings. This is because your interest has been hard at work earning you money.

What does this have to do with starting to save and invest early? Because the longer your investment period, the more compound interest works in your favour even if the returns are low.

Let us go back to our two people. Let’s say Person B manages to catch up with Person A. While the size of their nest eggs may look the same when they are 55, the composition of those nest eggs is very different:

Person A earns 12.8 million shillings in interest, while Person B earns 10.7 million in interest. Basically, by starting too late – even with the discipline to invest for the long term – you leave 2 million shillings of free money on the table. Another way to look at it, only 25% of Person A’s nest egg is their own contribution, while Person B’s nest egg is made up of 36% of their own contribution.

So please start today. Download The Money Box saving app, set a weekly goal and build your savings for a couple of months, then start setting that money aside for your long-term nest egg. One place to start your long term investing is the stock market, but before you set out to invest, check out our stocks articles.

Featured image: James Baldwin